Amazon (NASDAQ: AMZN) has come a long way since starting as an online book retailer out of Seattle nearly 30 years ago. The innovative company has expanded into multiple industries, from becoming a titan of e-commerce to leading the cloud market, developing space satellites, and venturing into grocery, gaming, consumer tech, and more.

Amazon’s success has seen its financials flourish, with its annual revenue, operating income, and free cash flow soaring over the past five years. Meanwhile, its market capitalization hit $1.9 trillion in 2024, making it the world’s sixth-most-valuable company and comparable to tech giants Alphabet, Nvidia, and Apple.

The company is on a promising growth path and seems nowhere near to hitting its ceiling as it continues to profit from the tailwinds of artificial intelligence (AI) and cloud computing. So, here’s why Amazon’s stock is a screaming buy right now.

It’s one of the most reliable long-term holds

One of the best reasons to invest in Amazon is its proven reliability under strain. An economic downturn in 2022 caused a marketwide sell-off, resulting in the Nasdaq Composite plunging 33% during the year. Retailers were hit particularly hard as inflation spikes forced consumers to cut discretionary spending. Shares in Amazon fell 50% in 2022 alongside steep profit declines in its e-commerce segments.

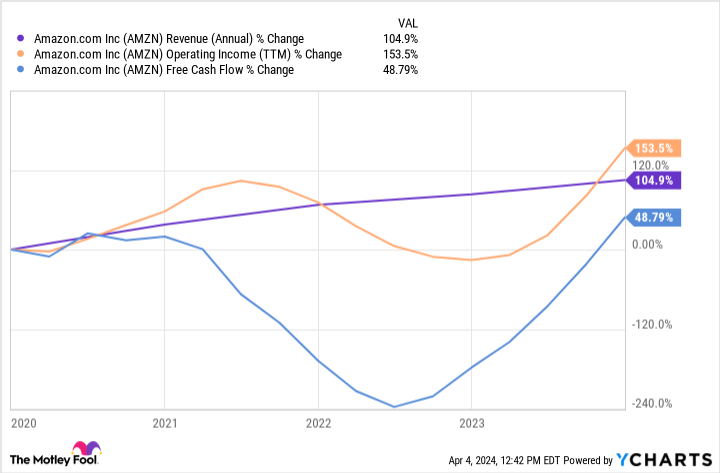

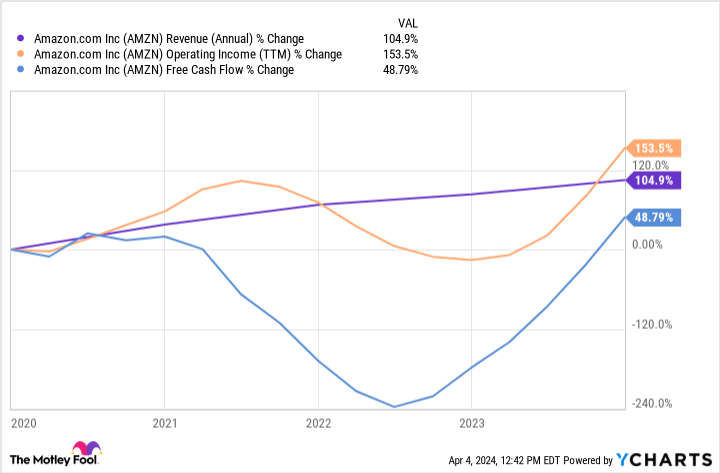

However, the company has made an impressive recovery, proving its reliability and resilience. In fiscal 2023, Amazon’s revenue rose 12% year over year to $575 billion, while operating income tripled to $37 billion.

A range of cost-cutting measures and easing inflation bolstered the company’s e-commerce business, and its free cash flow has skyrocketed 904% to $32 billion in the last 12 months.

Amazon’s performance over the last year highlights the importance of investing with a long-term mindset. Investors who sold the company’s stock in 2022 will not have benefited from its significant growth since then.

Promising upside over the next two years

According to Statista, the e-commerce market is projected to hit $3.6 trillion this year and expand at a compound annual growth rate (CAGR) of 10% until at least 2028. Amazon’s leading 38% market share in online retail therefore looks like the gift that will just keep on giving. The company’s role in the industry is paramount, proven by Walmart‘s second-largest share of just 6%.

However, Amazon’s biggest growth catalyst is easily its cloud platform, Amazon Web Services (AWS). In the fourth quarter of 2023, revenue from the platform rose 13% year over year to $24 billion. Meanwhile, AWS was responsible for 54% of the company’s operating income, despite earning the lowest portion of revenue among its three segments.

AWS gives Amazon a lucrative role in AI, a market projected to develop at a CAGR of 37% until at least 2030. As the world’s biggest cloud service provider, AWS has the potential to leverage its massive cloud data centers and steer the generative AI market.

So, it’s unsurprising that the cloud company is investing heavily in the budding sector. In 2023, AWS responded to increased demand for AI services by introducing a variety of new tools. The platform launched Bedrock, a program that helps customers build generative AI applications. It also unveiled CodeWhisperer, capable of generating code for developers, and HealthScribe, a tool that can transcribe patient-to-physician conversations.

Meanwhile, Amazon is even using AI to boost its retail site and announced an AI shopping assistant dubbed Rufus ahead of its latest earnings release.

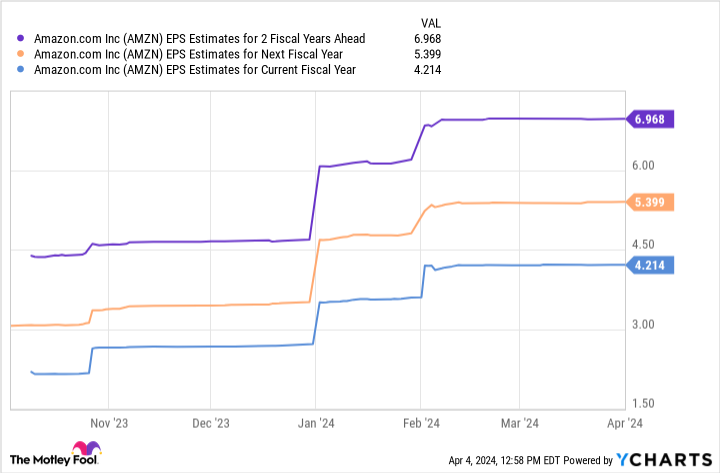

The tech giant is on a promising growth path, and earnings-per-share estimates seem to support its significant potential. The chart above indicates that Amazon’s earnings could achieve nearly $7 per share by fiscal 2026. When multiplying that by its forward price-to-earnings ratio of 44, you get a stock price of $308.

This projection would see Amazon’s stock rise 66% from its current value over the next two fiscal years. The company’s shares are a screaming buy right now and worth considering before its share price surges.

Should you invest $1,000 in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 4, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Dani Cook has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Nvidia, and Walmart. The Motley Fool has a disclosure policy.

Is Amazon Stock a Buy Now? was originally published by The Motley Fool